A little bit of knowledge is a dangerous thing

In this year of Trump, it has become fashionable to sneer at things you don’t understand. Like the EMH. TravisV sent me an example from the normally sensible Joe Weisenthal and Matthew Klein. It’s also a good example of why I don’t use Twitter. Lots of snarky comments that make a person look smart, but on closer examination merely show that the writer is witty.

JP Koning pointed out that I viewed yesterday’s market reaction as supporting the claim that the ECB actions helped European banks. Stocks rose on the announcement, and bank stocks rose especially sharply. I stand by that claim. Then Joe Weisenthal responded:

Almost all of the gains to which Sumner is referring to in this post were erased by the end of trading.

That’s true, but completely irrelevant. The problem here is that people don’t understand markets. Equity prices are always moving around. When you do an event study, what matters is the market response immediately after the announcement, not later in the day. You may “feel bad” that the stock rally didn’t last, but markets aren’t about feelings, they are about cold hard facts. In fact, if markets never reversed gains made early in the trading day, then the EMH would be entirely false. A few weeks back I was sent an email by a guy showing that previous BOJ surprises were followed by additional gains in the days and weeks ahead. Free money? Nope, right after making that observation, the Japanese markets reversed, and lost more than the initial gain from the BOJ’s recent decision to go negative. It’s just one coin flip after another.

Matthew Klein responds:

LOL

Joe Weisenthal responds:

Sumner’s insistence on using snap market reactions to judge policy a success or failure is head-scratching.

I’m honored that Joe thinks I invented “event studies”—that this is all my peculiar idea, but there are actually thousands of academic event studies. I’ve seen Paul Krugman favorably discuss the outcome of event studies. Then this was added to the Twitter thread, by someone else:

Sumner’s view is unfalsifiable. He will now say that ECB did not do enough.

Actually, event studies are among the most “falsifiable” of all academic studies. But notice how misleading this is. I actually did say the ECB needs to do more, but the commenter is giving readers the impression that I use that as an excuse for the decline in stocks later in the day. That is completely false, as it would not be consistent with the EMH. Yes, they need to do more, but my explanation for the decline in stocks later in the day was exactly the same explanation as the financial press provided. That’s right, publications like the Financial Times are apparently just as clueless as I am. I wonder why Weisenthal doesn’t say, “The mainstream financial press’s claim that asset prices reversed later in the day on Draghi’s comment that no further rate cuts were likely was head-scratching”? Perhaps he doesn’t know that this is what happened.

Asset markets are ruthlessly efficient. If they were not it would be easy to get rich. Just sell European bank stocks short after the “irrational” stock price run-up following an ECB announcement. Indeed I’d guess that even EMH skeptics like Robert Shiller mostly buy into the idea that markets respond immediately to new information. What reporters don’t understand is that the real world is messy. Asset prices change all the time. The standard deviation of daily changes in stock price indices is about 0.8%, which it pretty big (or at least it was last time I looked–for the 20th century). But the average change in any 10-minute interval is far smaller, so when you have a dramatic policy announcement, it’s often possible to see the market response–it really jumps out when you look at the data. And when you have many such announcements and the markets almost always respond as monetary theory would predict, then you can be especially confident.

Here is what apparently happened over the last couple of days:

1. Stocks rallied and the euro fell on the more stimulative than expected ECB announcement. Totally consistent with what we know about monetary policy.

2. Stocks fell sharply and the euro rallied on Draghi’s (perhaps misunderstood) statement at a press conference. Again, totally consistent with what we know about monetary policy

3. I don’t know why the markets reversed course again today, but James Alexander watches these things more closely than I do, and here’s what he reports:

There seems to have been a lot of public and private follow upon Friday from the ECB to reinforce their original, positively-taken, message.

“The European Central Bank embarked on a rearguard action to win over skeptical investors on Friday, a day after chief Mario Draghi unveiled a new stimulus package but blunted its impact by suggesting the ECB would not cut interest rates again.

A number of top ECB officials, both publicly and behind the scenes, spoke out in support of the measures Draghi announced on Thursday although some recognized the ECB had muddled its message to financial markets.”

http://reut.rs/1U6EeID

I have absolutely no idea whether that Reuters story is right or wrong, but it’s the sort of information that moves markets all the time. And markets should react to that sort of information, if it sends signals about future policy intentions. I’m sorry it’s so complicated, but that’s the world we live in.

Unfortunately, not all policy experiments are perfectly clean. In the old days you could look at fed funds futures prices, and then see if the Fed cut rates more or less than expected. The event studies were highly reliable. I admit that announcements are now somewhat more complex, but let’s not throw the baby out with the bathwater; they are still far better than any other method. What’s the alternative, wait 6 months and see what happens to the macroeconomy? Really? Like we know what the macroeconomy would have looked like if the decision had been a few basis points loser or tighter? That’s ridiculous.

This skepticism about market efficiency was one cause of the Great Recession (Joe’s probably thinking “Good Lord, Sumner’s now blaming me for the Great Recession, he really needs to take his meds.”) The Fed scoffed at market predictions of sharply lower inflation, right after Lehman failed. The markets were right and the Fed blew it.

Markets may look crazy, but only in the sense that an extraterrestrial being that was 100 times as smart as you or I would seem crazy. Asset prices move around all the time because the future is highly uncertain, and seemingly innocuous comments (like Draghi’s suggestion that no more rate cuts are expected) are actually very consequential.

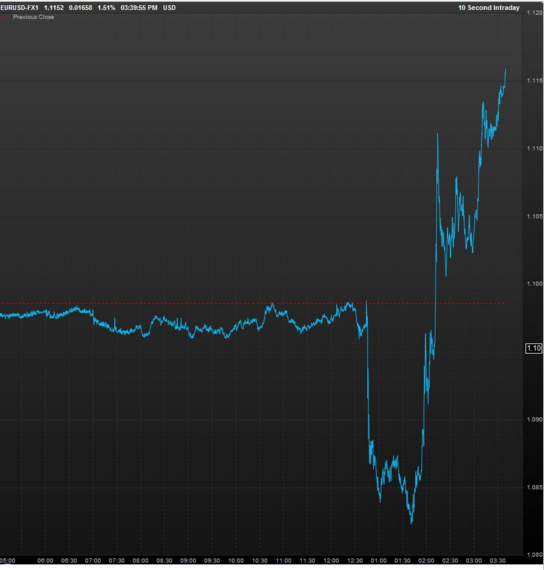

If the ECB skeptics are correct, and market movements are just so much noise, then I must be hallucinating to claim I can connect any given market movement to a specific policy announcement. OK, then take a look at the graph below, showing the value of the euro against the dollar, which is from Timothy Lee’s excellent Vox story on the day’s events. Suppose you didn’t know what time of day the ECB made it’s initial announcement and also the time when Draghi said this was going to be the final rate cut. Do you think you could guess, just from the graph? Maybe I’m hallucinating, but I think I see a meaningful fall in the euro at about 12:45, and a big jump just before 2PM. Gee, I wonder what those correspond to? It turns out the original ECB announcement was at 12:45. And Draghi’s statement that it was the final rate cut was at 1:56:30—just before 2pm. Huge market moves right after important new information. What an astounding coincidence!! After all, event studies are useless, right? Asset prices are just random noise.

PS. People are always telling me to get on Twitter. This is a perfect example of why I prefer blogging. You can have the sort of serious discussion in blogs that’s just not possible in 140 characters.

Tags:

11. March 2016 at 19:18

Good post. I don’t take market efficiency as far as Sumner does, but markets are the aggregate wisdom of an important part of the moneyed population combined into a number. Knowledgeable people can do better than markets in a lot of areas, but the ignorant should pay attention. And regarding the economy, it’s all too easy to be ignorant.

“If they were not it would be easy to get rich.”

-Not rich; richer. If the market is inefficient, it’s probably small enough for you to correct its irrational prices, which ruins the whole point of you being in the market.

I hate Twitter. It has poor JavaScript and is one of the worst mediums of serious dialogue. So far, I’ve only used it to retweet things others said, have a painful-as-hell conversation with pseudoerasmus, and live-tweet the #DemDebate.

11. March 2016 at 20:06

“The problem here is that people don’t understand markets. Equity prices are always moving around. When you do an event study, what matters is the market response immediately after the announcement, not later in the day.”

No, that is a theoretical claim derived from the fact that your economic framework is GENERAL EQUILIBRIUM. This framework focuses on final states of rest, as all mathematical models are so focused. You then arrogate this presumption as if it were tenable in the real world.

The reason why “right after the announcement” is being proposed as “the only thing that matters” is that it is the closest to the general equilibrium final state of rest. In other words, an announcement is made, and because the general equilibrium framework does not not tolerate any consideration of any market process, time, learning, or information dissemination, the smallest increment of time is the maximum time the model can accommodate, if it can even accommodate it.

Therefore we are told that an unrealistic model is somehow reality itself. That a particular change in information must have almost instantaneous effects.

The truth of course is that any given announcement does not have instanteous effects, because the price of a stock is the combined knowledge of a large number of individuals. Potentially millions. The demand that we all present in the purchasing of stocks today, can be influenced by the activities preceded by announcements made in the past. Our activities affect the price of stocks.

For example, pension funds that take time to digest new information and hold votes to decide portfolio rebalancing have a non-zero effect on tock prices. It is simply absurd to claim that the few speculators who trade very soon after a central bank announcement are the ONLY individuals whose activities have any effect on stock prices the information of which was a factor in their investment decisions. Stock prices are not merely a function of speculators who monitor central bank announcements by the minute. Stock prices are a function of EVERYONE who offers a demand for them. And if you weren’t born yesterday, you would know that everyone who makes up the investor population have significantly different reaction times, learning times, and investment decision timeframes.

When you see stocks prices swing up after an announcement and then soon after that you see prices going back down, it is absolutely wrong to claim that the initial run up was caused by the announcement and then the subsequent decline was caused by something else. How anti-empirical! Have you actually asked or inquired about the investors who bought and sold later on during the fall for why they agreed to those lower prices? Of course you didn’t! You just assumed that the subsequent fall was caused by something else. And why? Because that is what your theory tells you to do. It wasn’t reality that told you to think that.

Has it every occurred to you that maybe, just maybe, it is possible that the speculators who set the initially higher prices after the announcement, were “wrong” about what the ultimate outcome would be, an outcome which is the combined effect of more than just the speculators? That the initial speculators bid the prices a little too high, such that subsequent speculation (which could very well include the initial population of speculators) bid the price back down to what is a different interpretation of the same announcement? That the subsequent fall was caused by the announcement plus the initial reaction, and thus not independent from the announcement? In other words, that the subsequent fall was the effect of the announcement given the initial reaction?

As good as speculators are, they cannot predict their own future speculation, let alone the speculation of other investors. Think of an auction. If during the bidding process the announcer suddenly announced that the artwork last sold for a heftier sum than what the bidders expected, such that there are some passionate bidders who immediately throw their arm up and bid double the price, do you honestly believe that this initial bid is the only bid influenced by the announcement? There could be other bidders who react to the announcement differently and given the initial doubled bid, could refuse to buy at such a high price, and assuming the artwork is resold, it is possible the price could be lower than what the initial bidder thought would occur later on. So the price falls to a different price. THAT lower price is STILL influenced by the announcer’s announcement. Just because these series of bids are for a lower price than right after the announcement, does not permit you to assert that the cause must have been something other than the announcement, or that the initial rise is the only effect of the announcement and the subsequent lower price had nothing to do with the announcement.

To repeat, when you claim that the only thing that matters is the seconds or minutes after an announcement, what you are actually saying is that the only thing that your general equilibrium framework can accommodate is the immediate moment only. You are making a claim about the structure of your theory, nothing more.

11. March 2016 at 20:20

There’s only one cause for the ECB panic, and they were moderately successful. 100bp is 100% success.

http://www.boursorama.com/bourse/taux/cds-CDS_5A_DEUTSCHE_BANK-3xDB

11. March 2016 at 20:49

Excellent post, despite the gratuitous Trump-bash in the lead.

Print more money, unzone property, embrace Full Tilt Boogie Boom Times in Fat City.

11. March 2016 at 21:38

Twitter is useful for inciting riots.

I suggest you post a video of Chinese-Mexican Muslim migrants stabbing your book. Make sure to include a Buy-It-Now Amazon link.

11. March 2016 at 22:19

“You can have the sort of serious discussion in blogs that’s just not possible in 140 characters.”

Ahem… pussy crusher… sorry, just clearing my throat.

11. March 2016 at 22:32

O/T: Scott, did you know you had a new convert?

“Furthermore, out of spite, I am now a Market Monetarist. …they are a much better class of people.”

11. March 2016 at 22:50

The intra-press conference moves are even more interesting than you suspected. It looks like the pause in the snap-back rise in the Euro came when Draghi was asked the question whether the inflation target was symmetrical and his answer seemed to almost embrace level targeting. And also when giving his not too hostile thoughts on helicopter money, something he simultaneously claimed the ECB had not thought about. The rally resumed on his reading out his aides hastily botched together “clarification” that rates would not go lower. EMH rules!

It was like watching in-play betting markets during a football (ie soccer) match, with odds on the result changing dramatically as the goals go in. EMH rules there, too.

12. March 2016 at 00:29

Great post. Sometimes it’s hopeless how people ignore clear evidence.

I have been having a hard time explaining that Japan’s stocks fell after the initial rally following the 29th Jan. BOJ decision to introduce negative rates.

The market fell as soon as the BOJ began making clear that the rate will be charged on a very small proportion of the excess reserves.

The story background is the same. There is a lot resistance in Japan against negative rates – and BOJ official soon after the decision started to “appease” critics of negative rates that “it’s not that bad, we are not really going to charge you interest, don’t worry, very little will change”.

Markets began to rally again only after BOJ Deputy Governor Hiroshi Nakaso on 12th Feb. in NY made clear that there is still “no limit” to QE and that BOJ can cut rates further into negative territory, and that those who think the BOJ has reached its limit are “wrong”.

In short:

1) Nikkei rose when the initial announcement was made

2) Fell when BOJ started blurring the message

3) Rose again when BOJ corrected the message

It’s funny how many people find it so difficult to see these things. That’s what’s “head-scratching”…

12. March 2016 at 01:40

On the matter of Twitter, Mr Cameron PM has a view.

https://www.youtube.com/watch?v=d3Mrfut-FSw

12. March 2016 at 06:07

–CUT AND PASTE OF MAJOR FREEDOM’S POST HERE — I adopt it in its entirety.

Sumner: “In fact, if markets never reversed gains made early in the trading day, then the EMH would be entirely false. ” – absurd, Sumner is making the claim that is absurd. What form of the EMH is Sumner saying this is true for? The weak, semi-strong, or strong form? It seems Sumner is not claiming the strong form, which would not have a stock change in price on any announcement, since the announcement by definition must have been drafted in private and it would have already influenced the stock price. Thus Sumner is relying on the weak or semi-strong form EMH, see: http://www.investopedia.com/exam-guide/cfa-level-1/securities-markets/weak-semistrong-strong-emh-efficient-market-hypothesis.asp As such, Sumner’s logic is absurd since it implies an investor could make money on any new information by relying on a ‘regression to the mean’ argument for the stock price, knowing later in the day it will revert back to its old, pre-annoucement level. As such, this Sumner thesis violates the EMH.

Does this man get paid for anything he writes out of taxpayer money? If so, I want my money back! (I don’t pay US taxes, being offshore, but it’s the principle of the matter).

12. March 2016 at 07:05

I still wonder how EMH and The Donald go together.

A lot of groups seem to have problems to see Trump for what he *really* is according to quite a lot of guys (including Scott). How do we bring this together with EMH? In what way is a voting market different from any other market? Why should EMH not apply in a voting market?

And who are the real fascists by the way:

“Trump represents everything America is not and everything Chicago is not,” said Kamran Siddiqui, 20, a student at the school who was among those celebrating. “We came in here and we wanted to shut this down. Because this is a great city and we don’t want to let that person in here.”

…

Many of the protesters in Chicago said they were there to specifically to stop Trump from speaking.

http://nypost.com/2016/03/11/trump-calls-off-chicago-rally-due-to-security-concerns-amid-mass-protests/

The pictures are quite telling, too. (The “protesters” are wearing Bernie badges and other stuff). And this is an AP story by the way. Just for people who think it’s a NYP hack story.

12. March 2016 at 07:38

I agree that Weisenthal’s output is reliably interesting, but Matthew Klein seems to regurgitate the views of his sources. He is closer to Michael Lewis than to Weisenthal, except that, rather than being an exceptional writer, he produces fantastic charts.

12. March 2016 at 08:01

‘In what way is a voting market different from any other market? Why should EMH not apply in a voting market?’

Easy, in economic markets people are trading. Giving up something in order to receive something. That tends to concentrate the mind wonderfully with regard to value.

In voting that is completely absent.

12. March 2016 at 08:46

I have a very general question on EMH. Wikipedia describes it as:

‘In financial economics, the efficient-market hypothesis (EMH) states that asset prices fully reflect all available information. A direct implication is that it is impossible to “beat the market” consistently on a risk-adjusted basis since market prices should only react to new information or changes in discount rates (the latter may be predictable or unpredictable).’

I can understand that stock prices do indeed reflect all available information and will chnage quickly when new information (like unexpected CB announcements) appears. But why does that mean ‘it is impossible to “beat the market” consistently’ ? Given a set of data about something, won’t some people just be systematically better at interpretation and reacting to it than others ? When a good chess player plays a bad chess player, they both have the same information at any point in time, but the good player nearly always wins. Why isn’t it the same in the game of stock-picking ?

12. March 2016 at 09:04

Ray Lopez, I don’t see how you get from Maj Freedom’s post to yours. He makes some valid points though I think he’s underestimating the sophistication of the market. Your post, however, completely misses Scott’s point – he’s not saying that after shocks there is mean reversion, he’s saying after shocks there’s unpredictable movements that are as likely to be up or down, and when they go down it’s not because the shock was erased, it’s because markets move up and down. Obviously you have some understanding of the EMH but you seem to be willfully misunderstanding Scott just to attack him.

12. March 2016 at 09:42

Since I spent most of my career as a professional trader, perhaps I can try to clear up some misconceptions here regarding efficient markets. It is probably best to think of financial markets as very efficient, but not perfectly so, and to think of asset prices as determined by an amalgamation of the expectations of market participants; prices change when expectations change.

To Major.Freedom’s argument: I don’t think it is right to focus on different reaction times of different participants. If some news is released, like the ECB announcement, short-term traders can largely anticipate the reactions of other market participants with slower reaction times. So in practice the market reaction to such news typically is instantaneous.

To Ray’s remark about semi-strong EMH: I don’t follow the logic of your criticism. And your tone seems unduly harsh given that Sumner is just explaining some uncontroversial notions of how markets react to news.

To Market Fiscalist: You bring up some interesting points. If you assume that markets are perfectly efficient, then the prices of assets will fully reflect all available information, so a knowledgeable investor will not be able to consistently outperform a less knowledgeable investor. And in practice: Yes it is very hard to consistently outperform the market. Some investors have been able to exploit persistent market inefficiencies, but it is becoming increasingly more difficult to do so. Outperformance (“alpha”) has progressively become harder to achieve. There is a short book by Swedroe and Berkin, “The Incredible Shrinking Alpha” which has a nice discussion of this.

12. March 2016 at 09:49

Twitter is an incendiary communications medium. It acts as a high-pass filter, attenuating voices of reason and amplifying the shrill residual.

It’s not a coincidence that Bernie and Trump happen the first election cycle after Twitter goes mainstream.

#AmericanSpring

It’s also why Vox was so offensive trying to pin Trump on the Conservative movement; it’s the typical msm strategy of caricaturing their ideological opponents.

The Chicago rumble last night was a left-wing twitter mob carrying Bernie signs and Mexican flags to a Trump rally. Off-the-record, many said their purpose was to shut down the Trump rally. Several had a chance to speak on national TV, however, and merely stated they were unwilling say the purpose of their mob on national TV.

All they succeeded in doing was silencing Kasich and Cruz, and turning the evening news into Trumpvision TV.

12. March 2016 at 09:55

This market denialism is especially puzzling when talking about market expectations, which play an important role in monetary policy at the zero rate bound. It’s one thing to question whether inflation expectations in TIPS spreads, for example, predict inflation better than some other method. But, some people seem to doubt whether inflation expectations embedded in market prices reflect the markets’ expectations. How could they not? If market inflation expectations change in response to a Fed announcement then, by definition, that Fed announcement succeeded in changing expected inflation.

12. March 2016 at 10:33

The window around central bank meetings is most certainly not efficient. If fact, it is probably the largest market anomaly that exists. A very large portion of stock returns occur in the 24 hours prior to (but not including) the FOMC announcement. This chart shows the phenomenon through 2011…it has continued since (out of sample).

http://www.zerohedge.com/sites/default/files/images/user5/imageroot/2012/07/S%26P%20FOMC%20Impact.jpg

I would argue that relying on the market to be efficient in the window immediately following an incredibly inefficient window is not plausible.

12. March 2016 at 10:38

@Dennis – maybe I misread Sumner, who said: “In fact, if markets never reversed gains made early in the trading day, then the EMH would be entirely false.” – since I did not see the word “never”. But Sumner’s argument is thus strawman: he’s saying if the market never went down, it would refute EMH. But it would also no longer be a stock market, but a straight line upwards. Strawmen argument are typical for him.

12. March 2016 at 10:48

Bond and Equity markets reacted as if economy in the eurozone would be stronger moving forward. That is not at all inconsistent with markets believing Draghi will support growth moving forward … Maybe FX rates depende to much on rates, short rates, and bonds and equity markets look at overall, long term economic condition…

12. March 2016 at 12:38

Beckworth NGDP

http://ftalphaville.ft.com/2016/02/23/2154053/guest-post-the-fed-is-not-ready-for-the-next-recession/

12. March 2016 at 12:54

Harding, OK, but you could make a lot of money before “correcting” irrational pricing in the $/euro market. It’s very deep.

jknarr, Sorry, but what’s that all about?

Thanks Ben.

Steve, Good idea.

Thanks Tom.

Mikio, Thanks, that’s very helpful. Do you have any links to support all of that? (Unfortunately I’d need them in English)

Christian, I believe democracy is the best political system, due to the wisdom of crowds. For that reason, I expect Trump to lose.

Having said that, democracy is clearly less efficient than financial markets because it’s hard for individual voters to profit from the stupidity of other voters, whereas individual traders can profit from the stupidity of other traders. Thus bad people occasionally win, and indeed Trump might win.

Ray, Even more idiotic than usual, read Dennis.

Market fiscalist,

“Your theory is possible, but the EMH suggests that there are enough people who understand the correct model that deviations get quickly corrected. But again, it’s possible you are right. That’s the debate over Warren Buffett.

JCM, That seems about right to me—I’ve always argued the EMH is approximately true, but not exactly.

BC, Good point, that’s also my view.

Effem, Anomalies do not imply inefficiency, unless we can be confident the anomaly will persist in the future. I’m not confident.

12. March 2016 at 14:06

Hi Scott,

You said:

“Equity prices are always moving around. When you do an event study, what matters is the market response immediately after the announcement, not later in the day. You may ‘feel bad’ that the stock rally didn’t last, but markets aren’t about feelings, they are about cold hard facts. In fact, if markets never reversed gains made early in the trading day, then the EMH would be entirely false.”

I think this makes two errors.

First, the EMH is a statement of memorylessness of price movements (a random walk). On average, the market shouldn’t erase changes due to information shocks because that requires “memory”.

Second, in the case above the problem is not that the announcement was reversed but rather the “signal” (information shock) was much smaller than the “noise” (typical fluctuations in prices on larger time scales). It looks like Draghi’s announcement hasn’t been erased yet on a scale of hours:

http://finance.yahoo.com/echarts?s=EURUSD%3DX+Interactive#{“range”:”5d”,”allowChartStacking”:true}

But the size of this announcement is roughly the same size as other announcements — all of which have vanished in the noise at the scale of weeks to months. That means it doesn’t have any persistent effect — the day to day fluctuations of the market have more of an impact on ‘monetary policy’ (as measured with an exchange rate) than announcements from the central bank.

How do we interpret those daily moves, then? They tell us what agents in the market think (on average) about the effect of monetary policy on exchange rates. So we can conclude more agents trading in FX markets at the time of the announcement believe it was a loosening of monetary policy than think it was a tightening or no effect.

However, since no one has an economic theory of how markets work that is accurate enough to tell us how much exchange rates should fluctuate, these are just guesses. You’ve brought up the jellybean jar before — but this is like guessing the number of jellybeans in the jar when we don’t know how big the jar is!

In fact, there are models out there that say FX markets fluctuate too much (and ones that tell us they should fluctuate too much — e.g. Dornbusch overshooting). But maybe traders have the wrong model (or at least wrong magnitudes of effects) in their heads. Maybe CB announcements shouldn’t have an impact on exchange rates. Or maybe they should have the opposite effect. Since it is not definitively known, the market reaction is just a measurement of opinions.

12. March 2016 at 14:09

Scott, that’s Deutsche Bank 5 year credit default swap levels, en francaise. IMHO, the ECB panicked not because of any growth concern, but because of nasty growing stress in euro banks, DB being a particular bellwether. Going from 250bp to 140bp is a nice strong move that removes most margin stress at the banks.

The DB balance sheet is all that matters, and credit is a clean look at default – equity is “less smart” and more income statement-y in this regard.

12. March 2016 at 15:05

“short-term traders can largely anticipate the reactions of other market participants with slower reaction times. So in practice the market reaction to such news typically is instantaneous.”

So-so, often the big initial moves are on such thin volume because only an idiot chases the news tape. I always prefer to see confirmation with volume. Too many times I tried covering shorts on big fast down moves or longs on big fast up moves only to find vapor. Then right back to unchanged or the reverse…

I think people seem to have the misconception that you can just get long or short or flat instantaneously and don’t understand how much time and work it is takes get in and out of large positions. It’s a whole other skill set in itself…

12. March 2016 at 17:20

Fascinating to think of the market as a hyperintelligent alien. Great post.

12. March 2016 at 20:07

Let’s see if Sumner responds to physicist-cum-economist Jason Smith, who essentially is repeating Major Freedom’s major argument (and he’s right, namely there’s a time lag to shocks as more and more people respond to any information in the shock). Run away.

12. March 2016 at 20:52

@ssumner

-Yeah, but I don’t know too much about the Euro.

“Christian, I believe democracy is the best political system, due to the wisdom of crowds. For that reason, I expect Trump to lose.”

-The “wisdom of crowds” elected Chavez, the Kirchners, and Papandreou.

I expect Trump to win the general election due to his strong primary victory in Virginia, as well as the handicaps of Hillary Clinton. To win the general election, Trump needs to win only the states Romney won (easy) as well as Ohio, Virginia, and Florida. We’ll see how he performs in Ohio and Florida (which I think he’ll win, though Ohio is a wildcard, and Florida has a closed primary, which helps Cruz, and lots of Hispanics, which helps the Establishment). If he wins the vast majority of counties and the plurality of the popular vote in both state primaries, his chances of winning the general election are good (better than 50%). Trump’s Twitter and ad war against Hillary Clinton, combined with a strong desire among Middle Americans to Take Our Country Back from eight years of Kenyan-American Democrat misrule will surely help propel Trump to vote margins higher than McCain, and probably Romney.

12. March 2016 at 21:33

I believe less is more strategy is still effective in today’s some market.(anti-EMH model)

https://hbr.org/2014/06/instinct-can-beat-analytical-thinking/

I only know the name Trump and Hillary. So, I guess the next president will be one of the two.(the Hypermind prediction market)

Market(‘s characteristic) saves your brain’s computing resources.

Just believe EMH, think how to violate EMH.(?)

Anyway, I see the market still underestimate Abe-san’s will.

There will be Ise-Shima summit. I enjoy to see what will be happen.

(Nothing could be happen)

12. March 2016 at 23:49

Dennis,

Yours was by far the best comment.

13. March 2016 at 01:32

In what way is a voting market different from any other market? Why should EMH not apply in a voting market?’

“Easy, in economic markets people are trading. Giving up something in order to receive something. That tends to concentrate the mind wonderfully with regard to value.”

Yep, and you can suck at the former and still be allowed to keep voting… trading markets have self regulating moron removal filters built into them.

13. March 2016 at 03:19

Scott,

Both market moves make sense. The mystery is why second is larger than the first.

13. March 2016 at 08:25

democracy is clearly less efficient than financial markets because it’s hard for individual voters to profit from the stupidity of other voters, whereas individual traders can profit from the stupidity of other traders.

That’s the first good, logical sounding explanation I read regarding this topic. Thank you very much.

13. March 2016 at 14:34

I figured H. L. Mencken would have something to say about democracy… I wasn’t disappointed (lots of quotes!). E.g.

“Democracy is a pathetic belief in the collective wisdom of individual ignorance.”

13. March 2016 at 15:51

Jason, You said:

“First, the EMH is a statement of memorylessness of price movements (a random walk). On average, the market shouldn’t erase changes due to information shocks because that requires “memory”.”

I agree, and nothing I said contradicts this.

You said:

“Second, in the case above the problem is not that the announcement was reversed but rather the “signal” (information shock) was much smaller than the “noise” (typical fluctuations in prices on larger time scales).”

Not at all. Look at the fluctuations before the 12:45 announcement, and the move in the 10 minutes after. It’s easy to spot the market impact of the announcement against the background noise.

Harding, You said:

“The “wisdom of crowds” elected Chavez, the Kirchners, and Papandreou.

That’s all you’ve got? What would a list of leaders picked the other way (non-wisdom of crowds) look like? The Hitler of the late 1930s, Mao, Stalin, Lenin, Pol Pot, the three Kims, Idi Amin, Saddam, Mugabe, etc. And you talk about Kirchner? Seriously?

Vaidas, Maybe because the expected future path of policy is more important than the current setting.

Tom, Replace pathetic with “insightful” and he’s exactly right. BTW, the idea that Tom Brown can think is the pathetic belief that a bunch of dumb individual brain cells in Toms head can produce great insights by working together.

13. March 2016 at 16:00

Scott, touché. But your quarrel is with Mencken, not me. BTW, I looked at about a dozen quotes from him about democracy, and I don’t think I found one that was favorable. I prefer P.J. O’Rourke:

“The Democrats are the party that says government will make you smarter, taller, richer, and remove the crabgrass on your lawn. Republicans are the party that says government doesn’t work, and then they get elected and prove it.”

13. March 2016 at 16:15

@Tom Brown

So at least the GOP proves that their theory is true.

13. March 2016 at 16:42

“And you talk about Kirchner? Seriously?”

-Well, early 1930s Hitler and Francisco Macías Nguema came to power via rather democratic means.

“That’s all you’ve got? What would a list of leaders picked the other way (non-wisdom of crowds) look like?”

-It would also include the governments of Chiang Kai-Shek and his son, Deng Xiaoping and his successors (clearly superior to the various Indian and Mauritian governments of the time), the Lukashenko government (clearly superior to the Ukrainian governments of the time), the Brazilian and Greek juntas in the early 1970s (clearly superior economic record to later democratic governments in those countries), the Pinochet government, and the Franco and Estado Novo governments. Sure, governments not picked by the wisdom of crowds tend to be more brutal and more variable in outcomes, but their outcomes are by no means always worse than those of democratic governments originating from comparable contexts.

13. March 2016 at 17:42

Well, early 1930s Hitler and Francisco Macías Nguema came to power via rather democratic means.

Hitler’s ascent required a collapse of will on the part of the German political establishment. The Nazis had no majority in the Reichstag and all but four ministers in his cabinet were professionals without party affiliation. The context of that was the enormous stress of the loss of the war and serial economic disasters. As for Equatorial Guinea, it had no history of any kind of electoral politics, it was a hopeless amalgamation of two incompatible territories, and local population may have been Africa’s most primitive at the time. Robert Klitgaard’s account of dealing with Equatorial Guinea’s politicians post-Macias is instructive (though they did have the advantage of not being psychopathic monsters).

13. March 2016 at 17:44

But your quarrel is with Mencken,

Mencken was a talented wordsmith. He wasn’t a fountainhead of wisdom about social relations.

13. March 2016 at 17:53

and then they get elected and prove it.”

The Republicans have controlled the federal executive and federal legislature in tandem for just north of six years since 1930. The president had no legislative agenda for two of those years. For the other four, they had a plurality in the House thin enough that their room for maneuver was quite constrained and no real majority in the Senate given the effects of the changes in parliamentary rules adopted ca. 1974 (cadillac filibusters and indefinite holds on nominees; from 1920 to 1970 the Senate averaged one filibuster a year).

13. March 2016 at 17:53

JCM:

“To Major.Freedom’s argument: I don’t think it is right to focus on different reaction times of different participants. If some news is released, like the ECB announcement, short-term traders can largely anticipate the reactions of other market participants with slower reaction times. So in practice the market reaction to such news typically is instantaneous.”

The short term traders are not anticipating what the reactions will be for long term traders. The short term traders anticipate the reactions of other short term traders.

I’ve got about 14 years of brokerage trade desk experience in my belt, and in my experience while we do try to anticipate the reactions of other traders, we try to anticipate the reactions of only those investors who will be going long or short as far as our own investment time horizons. We are not trying to anticipate the entire investor population, certainly not the day traders. We are trying to anticipate short term price fluctuations which are “largely” driven by other short term speculators.

Short term speculators do not “largely anticipate the reactions of other market participants with slower reaction times.” That is wishful thinking. If you as a trader were involved in such an activity, then you would not be a short term speculator. You would be a long term investor yourself who puts less weight on the day to day fluctuations.

Perhaps you have heard of the empirical evidence of “momentum investing”? Stocks actually do not “instantly” adjust to news announcements. There are adjustments made over time that take into account the reactions to the news announcements as another source of information, which is not a “different” piece of information apart from the announcements. THIS is the information I am claiming is being ignored by EMH.

13. March 2016 at 19:42

Twitter is a great way of linking to a post while including some very short commentary. Tyler’s daily links would be better as 6+ tweets.

For what you try to do, it’s not exactly a good medium. You could have a chart ant two sentences, maybe. Far narrower than a blog.

13. March 2016 at 20:12

“@Tom Brown

So at least the GOP proves that their theory is true.”

Well, OK… hard to distinguish from a self-fulfilling prophecy though, which is P.J.’s joke.

13. March 2016 at 23:42

One of the funny parts of this conversation about markets readjustment times to news is I think about how deeply ingrained into me it was to ignore watching or listening to any news. News was always a 0 to me.

14. March 2016 at 04:49

Harding, You said:

“Well, early 1930s Hitler and Francisco Macías Nguema came to power via rather democratic means.”

I said the Hitler of the late 1930s, who was far worse.

And democratic Taiwan is far superior to non-democratic mainland China, just as democratic India is superior to non-democratic (usually) Pakistan. Please don’t compare China and India, that’s apples and oranges.

If you look around the world, the evidence in favor of democracy is pretty overwhelming. What’s the most democratic country—obviously Switzerland. The least democratic? Hard to say, maybe North Korea. Hmmm, decisions, decisions . . .

(If you insist on comparing apples to oranges.)

14. March 2016 at 04:53

to non-democratic (usually) Pakistan.

Pakistan’s had parliamentary governments for all but 3 of the last 30 years, with varying degrees of military supervision.

14. March 2016 at 08:10

“Maybe because the expected future path of policy is more important than the current setting.”

But Draghi said he is done with rate cuts only, he said he is shifting an emphasis to QE instead. Sometimes I think that market reaction is a vote for the effectiveness of conventional interest rate policy versus the unconventional.

14. March 2016 at 08:23

Art, What bearing does that have on my statement?

Vaidas, Negative IOR is not conventional interest rate policy, it’s a policy that imposes a tax on reserves to reduce reserve demand. Conventional policy adjusts the monetary base to indirectly affect the fed funds rate.

Why is it strange that the markets would think two tools are more effective than one?

14. March 2016 at 08:49

@ E. Harding,

You left out maybe the best example: Park Chung Hee in South Korea.

14. March 2016 at 09:05

“If you look around the world, the evidence in favor of democracy is pretty overwhelming.”

-Only if you ignore all the failed ones. SE Europe, Latin America, Africa. Democracy works best with a naturally non-corrupt population, dictatorship is far more variable.

Pakistan is ambiguous, as it’s had cycles of dictatorship and democracy. You didn’t challenge any of my other examples (other than India v. China).

Jeff, you are correct.

“And democratic Taiwan is far superior to non-democratic mainland China,”

-Also the case before Taiwan’s democratic transition.

14. March 2016 at 10:28

Hi Scott,

You said:

“It’s easy to spot the market impact of the announcement against the background noise.”

That’s a time-scale dependent statement. It disappears in the scale of fluctuations over e.g. weeks. That sets a scale of the size of the impact of the announcement — it’s a noticeable shift on the time scale of hours, but it’s negligible on a time scale of weeks.

http://informationtransfereconomics.blogspot.com/2016/03/the-emh-and-evaporating-information.html

15. March 2016 at 09:52

Harding, You are being disingenuous. Compare all the world’s democracies to all the non-democracies, it’s not even close. Now of course that’s not holding other things constant, but neither are your posts.

Jason, Well these policy shocks are small, so of course the effects will seem less significant on a longer time scale.

16. March 2016 at 15:39

Hi Scott,

Agree with you on NIRP, but could you ever take seriously the idea that market context could affect the fidelity of such an event study? Is the signal always louder than the noise (and can that noise be caused by the same event as the signal)? or are all trades that move market prices always and everywhere a reflection of a change in the perceptions of fundamentals? Could it be possible that the time it takes for the market to digest new information is longer than the two minutes after it is announced?

Prices may well be the money-measured-conviction-weighted beliefs of the market but why should conviction and information necessarily have the same distribution at all times? They distribution is possible close enough on average, but surely not at all times, or even often enough to be sure that a a single observation event study can be relied upon to elicit true beliefs.

In a world of rigid EMH, the optimal way to form beliefs is just to observe market reactions. Herding is rational and there is no information elicited and no trading – the world is too smooth. For trading to happen and for information to be elicited we need people with different beliefs and convictions in those beliefs. ‘We want to walk so we need friction. Back to the rough ground!’

16. March 2016 at 15:46

Relating the above to the ECB.. many hedge funds were long the front end of the German curve, the resulting unwinds after Draghis comments led the euro higher first and rippled through markets (perhaps in part due to the reflexive look-what-the-price-is-doing! reasoning described above)… This was more a reflection of positioning than fundamentals and those moves were retraced since.

25. March 2016 at 17:35

[…] temporary market movements, following a few posts on the topic written by Scott Sumner (see here, here and here). I eventually decided against, as I have written about the topic before and I just […]