It’s complicated

Macro is endlessly complicated, as I was reminded while reading Tyler Cowen’s recent post on his view of macroeconomics. One could write an entire book evaluating Tyler’s claims, but I’ll limit myself for now to this observation:

5b. Monetary stimulus to be effective needs to be applied very early in the job destruction process of a recession. It is much harder to put the pieces back together again, so urgency is of the essence.

I sort of agree, but there’s much more here than meets the eye, so let’s play around with it a little bit:

1. What does Tyler mean by monetary stimulus? Does he mean “concrete steppes”, such as money creation and/or cuts in the Fed funds target? Or does he mean an easier monetary policy as I would define it—higher expected NGDP growth?

2. In other words, there are two ways to read Tyler’s claim; that it’s hard to boost AD quickly when the economy is already sliding into a deep recession, or that even a quick and vigorous boost to AD will have limited impact on employment, in the short run. Both claims are defensible, but they are very different claims.

3. For instance, when the economy is deep into recession, the Wicksellian equilibrium interest rate is generally falling rapidly. That means a cut in the fed funds target may not effectively ease monetary policy. Using monetarist language, V may be falling and so a monetary injection may not boost M*V.

4. If NGDP is sharply boosted in a recession (and I believe it can be) then there’s also the “job-matching” problem. People who lose jobs typically are not re-employed at the same company. Thus RGDP may not rise, even if NGDP does.

5. On the other hand, the net change in employment, even during a recession, is quite small compared to the background rate of job creation and job destruction. I seem to recall that roughly 31 million jobs are created each year, and 30 million are destroyed. (Relying on memory, correct me if that’s wrong.) If so, then the job-matching problem is not likely to prevent a quick end to the recession, and vigorous recovery. Just do enough to stop the layoffs, and the flow of new jobs that is always occurring in the background will rapidly boost employment.

All of those perspectives barely scratch the surface of the issues raised by Tyler’s claim. Here’s another way of looking at it:

1. A sound monetary policy will not fix recessions, it will prevent them. That’s because recessions tend to occur when expected future NGDP (1 and 2 years forward) drops significantly. And that sort of drop reflects bad monetary policy. The way to stop a recession that has already begun is to prevent it from happening in the first place.

2. And no, I’m not simply making a “If I was headed to Vegas I wouldn’t start from here” snide remark, I am quite serious. A recession is a sustained drop in output, but it technically begins when output starts dropping. That means a recession can be prevented from occurring, even after it has started (indeed up to about the 6 months point.)

3. Here’s an exchange rate peg analogy. Suppose you are pegging exchange rates, and are asked how to react to a 10% fall in the value of the currency. What is the answer? My answer is, “don’t let it fall 10%.” But what if it does fall 10%? Then you try to punish the speculators by quickly pushing it back up again, so that the bears lose a lot of money. By analogy, the best solution is to have a monetary regime where expected NGDP growth always remains on target. But if it slips for some reason, then bring it back up immediately. Then there is the issue of how quickly actual NGDP responds to a recovery in NGDP expectations. I say “really fast” but can’t prove that. It would be an interesting hypothesis to test.

So far I’ve been hinting that Tyler’s claim is too simple, that perhaps a quick recovery via monetary stimulus is possible. But there’s a third way of looking at this issue, which tends to support Tyler’s claim:

1. If markets are efficient, then NGDP expectations are rational. If I’m right that recessions are caused by sharp declines in expected future NGDP, which then depresses current NGDP, then a quick recovery can only occur if the market forecast was wrong.

2. Now think about Tyler’s claim from the following perspective. How optimistic should we be that a monetary regime can solve problems that the market currently thinks it will fail to solve? An EMH fan like me would say, “not very optimistic at all.” If your policy regime is to “vigorously boost NGDP expectations whenever you go into recession”, then you should never go into a (demand-side) recession in the first place. It’s like if your policy were to immediately bring an exchange rate back to the peg anytime it fell more than 1%, then it should never fall 10%. If it does, your policy has already failed, or more precisely has already been expected to fail.

3. Most economists think in terms of; “What do we do at the zero bound?” I think that’s a really bad way of thinking about the problem, like discussing what to do if the bus is flying over the guardrail. You want a policy that avoids zero rates, by avoiding really low NGDP growth expectations. If you have a recession and/or a zero interest rate, it’s pretty clear your policy has failed. So I can’t blame Tyler for being really pessimistic about the prospects for monetary “rescue” at that point, it would require policymakers to be smarter than the market, which they ain’t.

To summarize, we have a recession because the market thinks a monetary rescue is really unlikely to occur. That doesn’t mean there is any technical barrier to a monetary rescue, but it does suggest that the institutional structure of the monetary policymaking process is not conducive to a quick recovery. So pessimism is in order, albeit perhaps for a slightly different reason from what most people assume.

Note that this analysis does not apply to the business cycles of the 1920s, 1940s or 1950s, when recoveries from recession were very quick. I don’t know why we don’t have those sorts of recoveries anymore (although of course I have theories). If elite macroeconomics were as successful as its practitioners would like us to believe, then we’d have an answer to this question; we’d know why recoveries have become agonizingly slow.

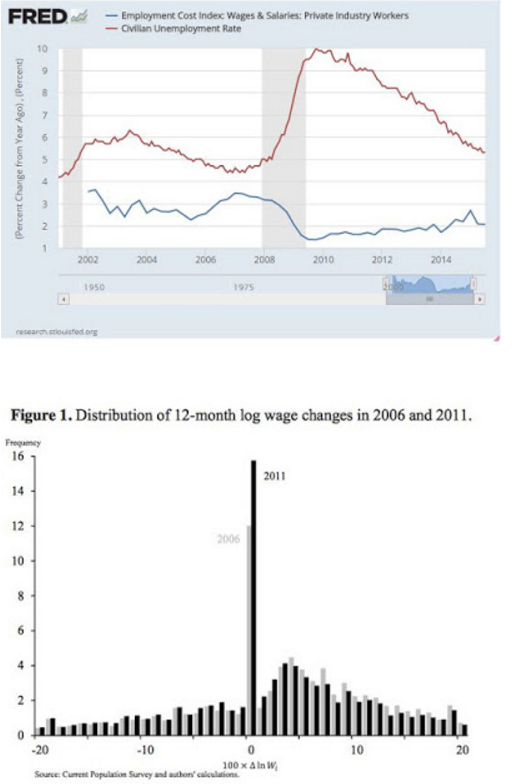

PS. I strongly disagree with Tyler’s point 5a on sticky wages, but will wait for the clarifying post he promises.

PPS. Lars Christensen will be doing a speaking tour in 2016. I strongly recommend that you book him for any topic other than “Why China will never be the largest economy in the world.”

PPPS. I hope people didn’t miss the excellent piece on the euro, by Matthew Klein.

PPPPS. Although I don’t agree with every single detail, I strongly support the general thrust of this Paul Krugman post on terrorism.